Who’s Leading the SAF Race? Leaders, Challengers, and Innovators in Technology Licensing

Time to read:

10

mins

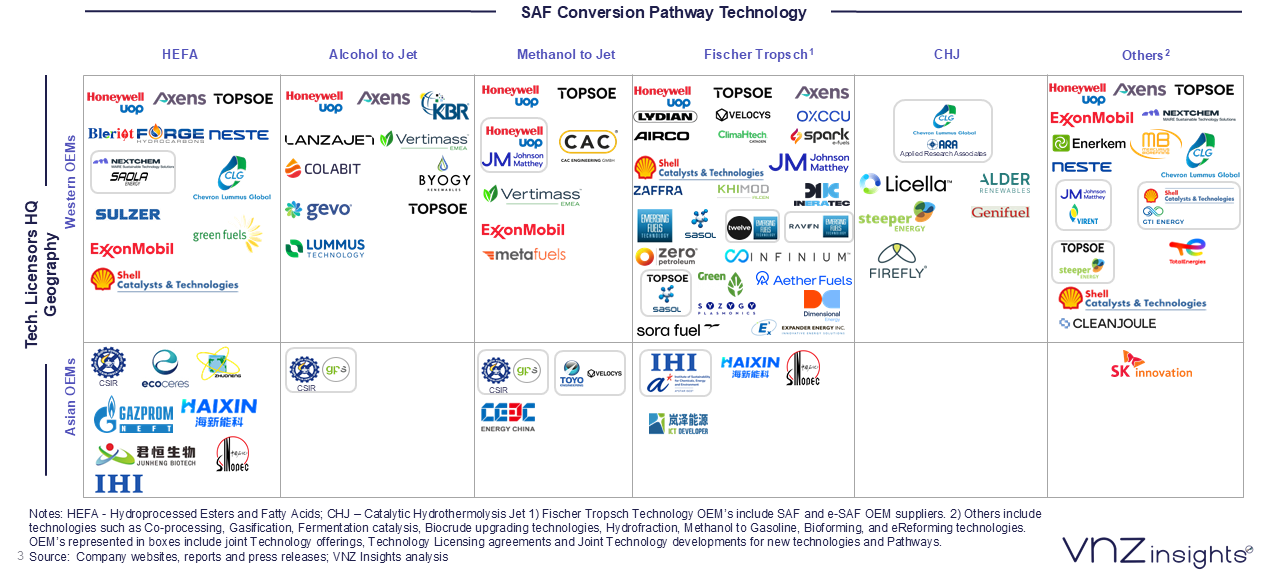

Sustainable Aviation Fuel (SAF) is transitioning from demonstration to early commercial scale. Six ASTM-approved pathways dominate the landscape: HEFA, FT, Co-processing, ATJ, CHJ, and MTJ. These pathways differ primarily in their feedstock dependence and scalability:

-

• Feedstock-specific (HEFA, CHJ/HTL): Optimized for defined inputs such as lipids or waste oils

-

• Feedstock-agnostic (FT, PtL/eSAF): Flexible inputs but highly sensitive to hydrogen and energy costs

-

• Feedstock-flexible (ATJ, MTJ): Adaptable but requires preprocessing

-

• Refinery-integrated (Co-processing): Low capex entry but constrained by blend limits

- Key takeaway:

-

The SAF technology licensing ecosystem is currently dominated by Western companies, reflecting early policy support and commercialization momentum in Europe and North America. However, Asian players are rapidly scaling through strategic partnerships and government-backed initiatives.

-

• Europe:

-

• North America:

Leads in commercialization and licensing scale, with key players including Honeywell UOP, LanzaJet, Chevron Lummus Global (CLG), Gevo, and KBR. Many operate as asset-light IP licensors, monetizing global deployment via engineering and licensing contracts.

-

• Asia:

Gaining momentum through state-backed refiners and integrated industrial players such as Sinopec, SK Innovation, and EcoCeres, supported by R&D institutions like CSIR and IHI. Partnerships such as TOYO–Velocys and CSIR–GPS Renewables are accelerating pilot-to-commercial transitions.

-

• Rest of the World:

Players like Sasol and Licella contribute through specialized technologies, particularly in FT and advanced biofuel segments.

- Key takeaway:

While Western firms retain technology leadership, Asia’s scale advantage and policy backing could significantly reshape the competitive landscape by 2030.

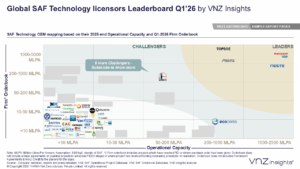

- THE LEADERBOARD

-

VNZ’s proprietary leaderboard identifies the leaders, challengers and innovators based on two key criteria- Operational capacity and Firm orderbook, which includes projects which have reached FID or where a purchase order has been given. Orderbook does not include Framework Agreements & MoU.

- Leaders:

- Challengers:

• EcoCeres, Sinopec, and LanzaJet are emerging challengers in the SAF market, expanding capacity through proprietary technologies and strategic project development. EcoCeres has commissioned SAF facilities, including EcoCeres Biochemical Technology and EcoCeres Malaysia, using its proprietary HEFA technology. Sinopec is strengthening its position in China through SAF pilot projects such as the Zhenhai Refining & Chemical and Zhungeer R&D Centre Gasification-FT, alongside a joint SAF project with TotalEnergies at Zhenhai Refining. LanzaJet, a spin-off of LanzaTech, is advancing Alcohol-to-Jet (ATJ) technology through its operational Freedom Pines Fuels facility and firm orders from projects, including Jet Zero – Project Ulysses and the UK II Dragon Project, among others.

- Innovators:

• Infinium, INERATEC, and Metafuels represent the next generation of SAF innovators, focused on scaling synthetic and e-fuel technologies. Infinium has raised over 1.1 bn USD to advance ultra-low-carbon eFuel and gas-to-liquid projects, including Project Roadrunner, Electrofuels France (ReuZe), and the Infinium-SMA eSAF Project. INERATEC specializes in modular power-to-liquid systems that convert renewable hydrogen and CO₂ into synthetic fuels and chemicals, having secured 215 mnUSD in funding to scale projects such as ERA Two, ERA Three, and Project BELair. Metafuels is developing its proprietary AeroBrew methanol-to-jet technology, having raised 41 mnUSD across five funding rounds, with a demonstration plant under development at the Paul Scherrer Institute in Switzerland and its first commercial e-SAF project, Turbe, progressing at the Port of Rotterdam.

-

The SAF market is evolving into a multi-pathway, multi-region ecosystem, where success will depend on more than just technology.

-

Key trends shaping the market through 2030:

-

• Shift from pilot projects to commercial deployment

-

• Rising importance of feedstock access and supply chains

-

• Increasing role of low-cost renewable hydrogen in eSAF pathways

-

• Growth of licensing-driven business models

-

• Stronger participation from Asian players backed by policy mandates

-

About the Report

This analysis is part of VNZ Insights’ report, “SAF Technology Licensors Landscape and Leaderboard,” covering 60+ global licensors.

-

The report evaluates:

-

• Technology pathways (HEFA, FT, ATJ, MTJ, CHJ, others)

-

• Geographic dynamics (Western vs. Asian players)

-

• Technology maturity (concept to commercial)

-

• Business models and licensing strategies

-

• Key trends and competitive positioning through 2030

This insight was powered by RFLN.

Want more insights like this?

Access live data, project trackers, and market intelligence built for OEMs, EPCs, and investors.

Download the insight/report:

Click here to DownloadSources-

https://vnzinsights.com/flagship-report/vnz-saf-technology-licensors-landscape-and-leaderboard-report/

Image Sources-

VNZ Insights