The 2025 Nuclear Funding Boom

Time to read:

10

mins

The nuclear energy sector is experiencing unprecedented investment momentum in 2025. Across fission, fusion, and supply chain infrastructure, the industry has mobilized approximately 5 bn USD in disclosed funding across 30 significant deals, signalling a decisive shift in how capital markets view nuclear energy's role in the global energy transition. This surge reflects growing confidence that advanced nuclear technologies that were once considered distant prospects are now rapidly advancing toward commercial reality. This article examines how and where capital is flowing within the nuclear ecosystem in 2025, drawing from VNZ Insight’s comprehensive 2025 Nuclear Deal Database.

Equity funding in nuclear industry hits 5 bn USD in 2025-

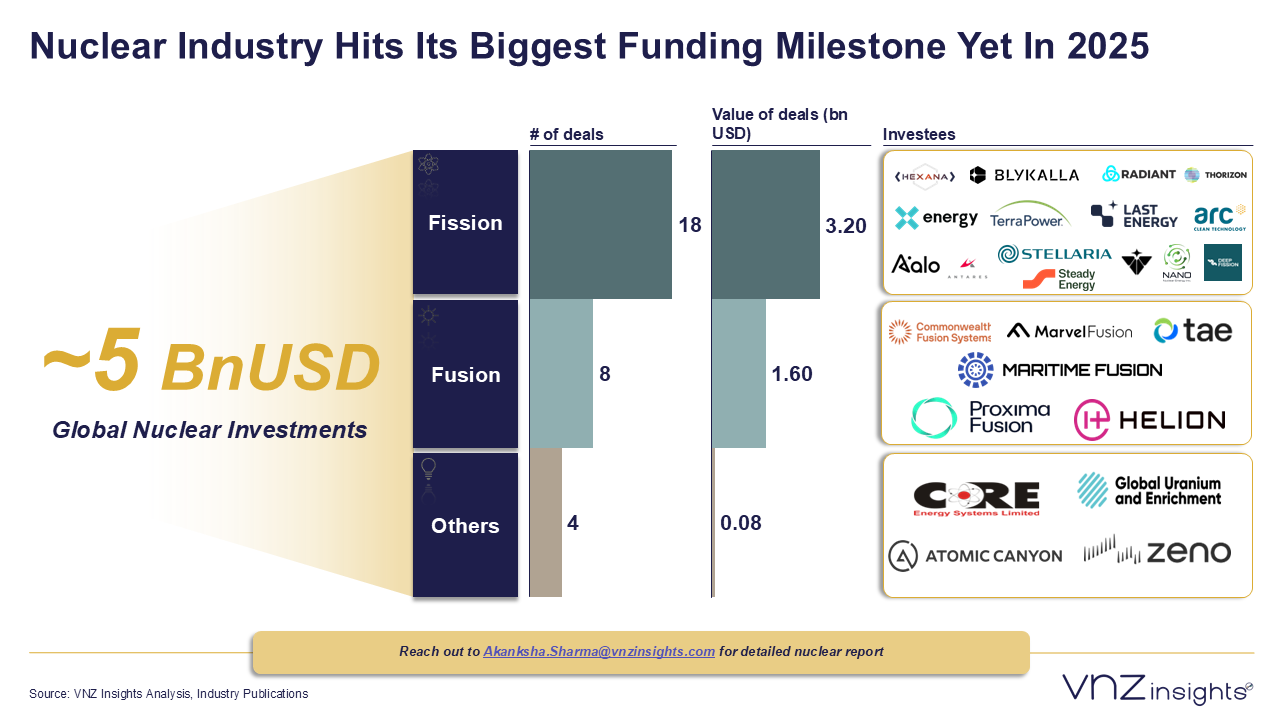

2025 marks a record year with the highest annual venture funding to date in the nuclear energy industry. 5 bn USD has been deployed across 30 investment deals, spanning advanced fission reactors, fusion demonstration projects, and nuclear supply chain infrastructure.

- • Fission technologies: 3.2 bn USD across 18 deals

- • Fusion technologies: 1.7 bn USD across 8 deals

- • Supply chain and other infrastructure: 83 mnUSD across 4 deals

-

The Investee Landscape: Market Consolidation and OEM Dominance

-

In 2025, nuclear investment was characterized by extreme consolidation. Rather than scattering capital across dozens of early-stage startups, investors coalesced around a select few hardware frontrunners, highlighting a clear preference for companies approaching commercial viability.

Out of the 25 unique companies that successfully raised funds, a staggering 76.1% (3.8 bn USD) was secured by just five entities: X-energy (1.4 mnUSD), Commonwealth Fusion Systems (863 mnUSD), TerraPower (650 mnUSD), Radiant Nuclear (465 mnUSD), Helion (425 mnUSD).

-

Late-stage rounds dominate the market

-

Series C, D, and later-stage rounds account for the majority of the capital deployment, indicating that investor focus has shifted decisively toward technologies with visible deployment pathways and de-risked business models. Helion's 425 mnUSD Series F and TAE Technologies' 150 mnUSD Series G highlight the rapid expansion of fusion technology within the nuclear industry.

Notably, early-stage and seed-stage funding remains consistent but modest in comparison. Early-stage deals like Proxima Fusion’s Series A (150 mnUSD), Valar Atomics' Series A (130 mnUSD), and Atomic Canyon’s seed funding (7 mnUSD) show continued venture appetite for promising architectures.

-

Global nuclear investment led by the US

-

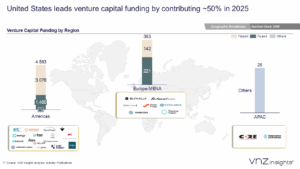

The U.S. continues to lead the global nuclear venture funding landscape. Of the nearly 5 bn USD tracked globally in 2025, 4.6 bn USD (over 92%) was captured by U.S.-based companies. Mega-rounds for American developers like X-energy, TerraPower, CFS, and Helion skewed the geographic distribution heavily toward North America, though European startups continue to see early-stage traction.

Germany leads European funding with Proxima Fusion's 130 mnEUR Series A in Munich, reflecting the region's commitment to fusion research. Sweden (Blykalla), Finland (Steady Energy) and the Netherlands (Thorizon) have attracted funding for advanced fission SMRs, supported by EU-backed investment programs like InvestEU and the European Innovation Council Fund.

Investments in the APAC region have come primarily from India and Australia, carving out a vital niche in localizing the nuclear supply chain with CORE Energy (Indian nuclear EPC company) 23 mnUSD round and Ubaryon securing 3.2 mnUSD backing from Urenco for advanced uranium processing.

-

Advanced Reactors capture the majority of capital

-

Within the fission sector, funding has concentrated heavily on advanced reactor designs that promise to reduce capital costs, improve operational flexibility, and accelerate deployment compared to conventional light-water reactors. High-Temperature Gas-Cooled Reactors led the pack, securing 2.1 bn in funding. Molten Salt Reactors followed with 697.7 mnUSD, while Sodium-Cooled Fast Reactors captured roughly 194 mnUSD.

Within the fusion sector, Tokamak architectures attracted the most capital (867.5 mnUSD), driven heavily by Commonwealth Fusion Systems. Field-Reversed Configuration technologies ranked second with 582.4 mnUSD, while Stellarator designs secured 167 mnUSD.

-

Strategic Investors and CVCs shape the landscape

-

Strategic investors played a major role in nuclear funding activity throughout 2025. While venture capital remains a dominant force in providing the equity required to develop capital-intensive reactor technologies, corporate venture capital (CVC) and industrial groups are aggressively entering the cap tables.

Major tech giants, motivated by the immense energy demands of AI data centres, are leading the charge—most notably Amazon's direct investment into X-energy and NVIDIA's NVentures backing fusion through CFS and fission through X-energy. Furthermore, massive consortiums of international industrial groups (including Mitsui & Co., Mitsubishi Corp., and JERA) are providing crucial supply-chain and financial backing to ensure these technologies can scale globally.

Government funding through entities like InvestEU, European Innovation Council Fund, and UK Atomic Energy Authority are increasingly backing advanced nuclear through large-scale loans, credit facilities, and strategic investments, reflecting the sector’s growing importance for energy security and national sovereignty.

Individual investors are increasingly funding fusion and nuclear supply chains, with tech founders and prominent investors backing major nuclear and fusion companies. For instance, CORE Energy secured a 23 mnUSD strategic round backed by Pankaj Prasoon and Ashish Kacholia to scale precision nuclear engineering in India. Similarly, massive fusion rounds continue to rely on the private wealth of tech founders and billionaires, with figures like Sam Altman and Dustin Moskovitz backing Helion, and Stanley Druckenmiller participating in the CFS mega-round.

-

The Critical Gap in the funding landscape

-

2025 represents a maturation moment for nuclear energy investment. The 5 bn USD deployed across 30 major deals demonstrates that nuclear is no longer a fringe bet but a mainstream energy transition strategy.

However, this industry is experiencing a "reactor-centric" funding bubble while critical enablers remain dramatically underfunded. The imbalance is unsustainable: reactor developers will race ahead of manufacturing capacity, supply chains will bottleneck, and deployment timelines will slip if supporting infrastructure gaps aren't addressed immediately.

This insight was powered by NFLN.

Want more insights like this?

Access live data, project trackers, and market intelligence built for OEMs, EPCs, and investors.

Download the insight/report:

Click here to DownloadSources-

VNZ Insights

Image Sources-

VNZ Insights